Stop overpaying the IRS! Learn how to maximize your real estate tax deductions in 2026, from mortgage interest secrets to the newly expanded SALT cap limits.

Table of Contents

I’ll never forget the first time I sat down to do my taxes after buying my first property. I had a shoebox full of receipts, a mounting sense of dread, and absolutely no idea that my leaking kitchen faucet was actually a “deductible repair.” Like many of you, I was terrified of the IRS, but even more terrified of leaving my hard-earned money on the table.

Real estate is often called the “ultimate tax haven,” but that’s only true if you actually know where the “havens” are hidden. Whether you are a homeowner just trying to make the mortgage pay off or a seasoned investor looking to shield your rental income, understanding real estate tax deductions is the difference between a stressful April and a celebratory one.

As we move through 2026, the landscape has shifted. We have new legislation like the “One Big Beautiful Bill” (OBBBA) that has tweaked everything from state and local tax caps to depreciation schedules. If you’re still using 2023’s logic, you’re probably overpaying. Let’s dive into the practical, real-world ways you can keep more of your equity where it belongs—in your pocket.

The Big Reset: Homeowner Deductions in 2026

If you live in the house you own, your primary goal is to lower your taxable income by “itemizing” your deductions. For many, the standard deduction is still the easiest route, but with the recent changes in 2026, itemizing is back in style for homeowners in high-value markets.

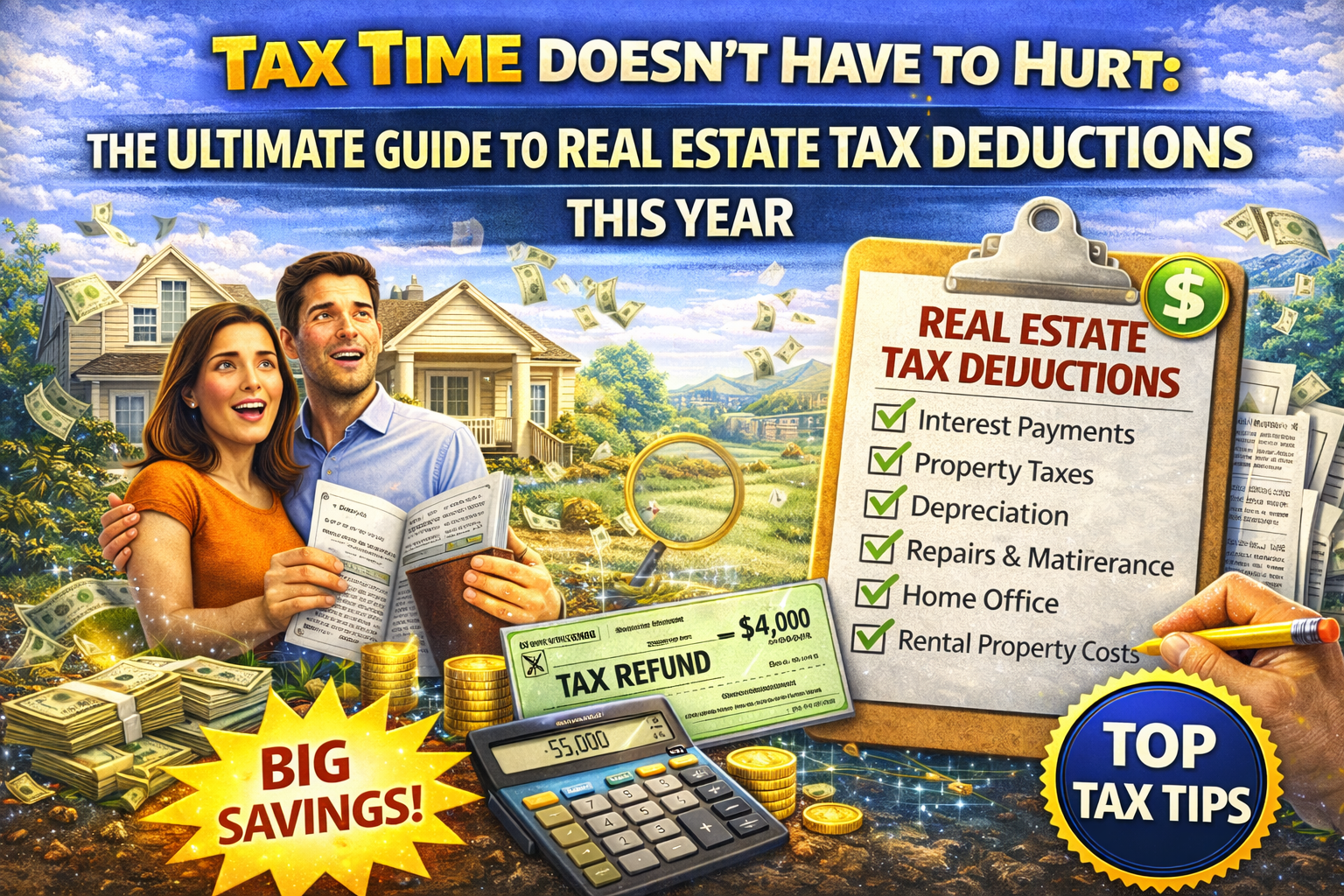

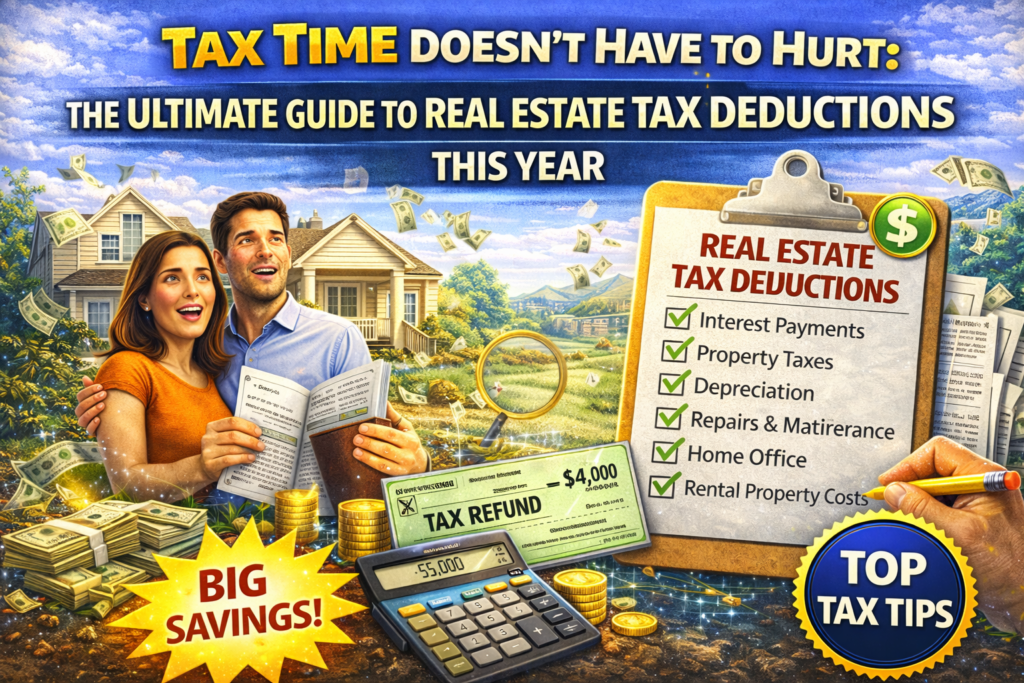

1. The Mortgage Interest Deduction

This is the “Old Reliable” of real estate tax deductions. You can deduct the interest you pay on up to $750,000 of mortgage debt ($375,000 if married filing separately). If you bought your home before December 16, 2017, you’re likely grandfathered into the older, higher limit of $1 million.

2. The SALT Cap Expansion: A Major Win

For years, homeowners in high-tax states felt “capped out” by the $10,000 limit on State and Local Tax (SALT) deductions. In 2026, things have changed. Under the OBBBA, the SALT cap has been significantly increased to $40,400 for individuals and joint filers (with a phase-down starting at a MAGI of $505,000). This means your property taxes and state income taxes finally have some room to breathe on your federal return.

3. Points and Closing Costs

Did you pay “points” to lower your interest rate when you bought or refinanced? Those are generally deductible as pre-paid interest. If it was for a purchase, you can often deduct them all in the year you paid them. If it was a refinance, you usually have to spread that deduction over the life of the loan.

Rental Property: The Investor’s Secret Weapon

If you are an investor, you aren’t just looking for a few write-offs; you are running a business. The IRS allows you to deduct almost every “ordinary and necessary” expense required to manage, conserve, or maintain your rental. This is where real estate tax deductions turn a modest rental into a cash-flow machine.

Depreciation: The “Paper Loss”

Depreciation is the king of real estate tax deductions. The IRS assumes that your building is slowly wearing out over 27.5 years (for residential) or 39 years (for commercial).

- Residential: You can deduct roughly 3.636% of the building’s value every year.

- Pro Tip: Land does not “wear out,” so you must subtract the land value from your cost basis before calculating depreciation.

Repairs vs. Improvements

This is where I see the most mistakes.

- Repairs: Fixing a broken window or painting a room is a “repair.” You can deduct the full cost in the year you pay for it.

- Improvements: Replacing the entire roof or adding a deck is an “improvement.” You must “capitalize” these and depreciate them over several years because they add value or extend the life of the property.

Pass-Through Entity Benefits (Section 199A)

If you hold your real estate in an LLC or as a sole proprietor, you may still be eligible for the Qualified Business Income (QBI) deduction. This allows you to deduct up to 20% of your qualified business income from your taxes, provided you meet certain “safe harbor” requirements regarding the hours you spend managing the properties.

Professional Fees and Travel

Don’t forget the “soft costs” of owning property. If you drive to your rental to collect rent or meet a contractor, that mileage is a deduction. If you pay a property management company to handle the headaches, their fees are 100% deductible.

Even the cost of this blog post (if you were paying for a tax-subscription service) or the fees you pay your CPA to prepare your Schedule E are legitimate real estate tax deductions.

FAQ Section

1. Can I deduct property taxes on a second home? Yes. You can deduct property taxes on as many homes as you own, provided the total amount of your state and local taxes stays within the 2026 SALT cap of $40,400.

2. Is my home office deductible if I own my house? Only if you are self-employed and use the space exclusively and regularly for business. If you are a W-2 employee working from home, the federal home office deduction is currently not available to you.

3. What happens to my deductions if I sell my rental property? You may have to deal with Depreciation Recapture. The IRS will want to tax the depreciation you claimed (or could have claimed) over the years at a rate of 25%. This is why many investors use a 1031 Exchange to defer those taxes into a new property.

4. Can I deduct the interest on a Home Equity Line of Credit (HELOC)? Only if the money was used to “buy, build, or substantially improve” the home that secures the loan. If you used your HELOC to buy a new car or pay for a wedding, that interest is not among your allowed real estate tax deductions.

5. Do I need to keep receipts for small repairs? Absolutely. In an audit, the IRS doesn’t care about your “best guess.” Keep digital copies of every receipt for materials, contractor labor, and even the lightbulbs you bought for the hallway.

6. What is the “14-Day Rule” for vacation rentals? If you rent out your personal vacation home for 14 days or less per year, you don’t even have to report that income to the IRS. However, you also can’t take any rental-specific real estate tax deductions for that period.

Conclusion

Tax laws are built to encourage property ownership and investment. The government wants you to provide housing and maintain your home, so they “reward” you with these provisions. But they won’t force you to take them—you have to be the one to claim them.

Whether it’s maximizing the newly expanded SALT cap or performing a cost-segregation study to speed up your depreciation, the goal is the same: reduce your taxable footprint so you can reinvest in your future. Real estate is a long game, and mastering real estate tax deductions is how you win it.